Good Morning,

I hope you had a great weekend. As we move into March, several key metal markets are stabilizing following recent volatility. However, aluminum and some nickel based alloys have shown continued increases in strength.

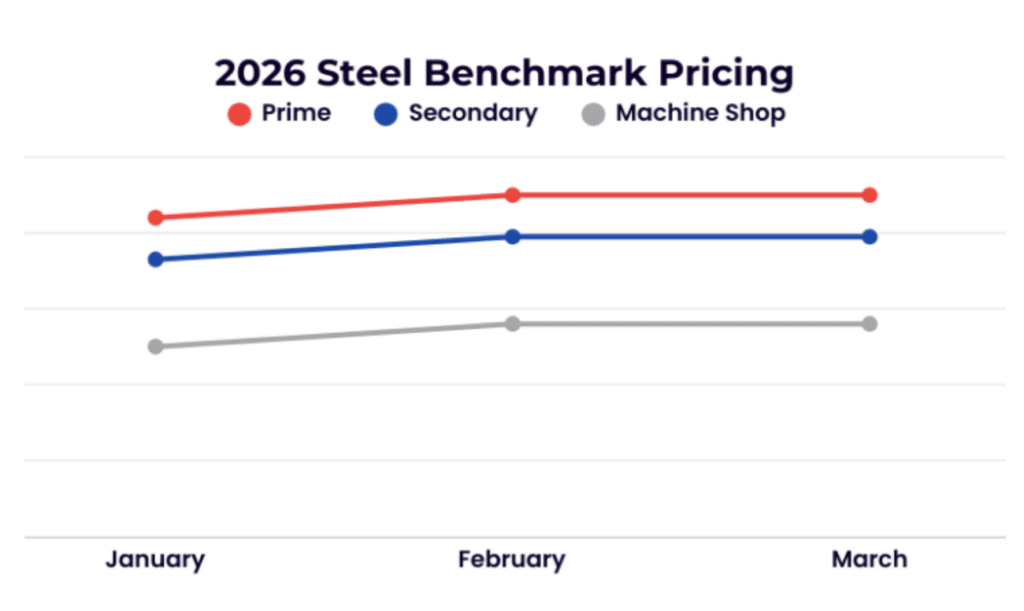

Steel

The U.S. steel scrap market remained steady in March. Supplier and mill delays from February created a supply-driven need for stability. Despite expectations of softening as winter conditions improved, many suppliers still faced February backlogs, limiting their flexibility to accept lower pricing.

Non-Ferrous

Aluminum prices increased sharply as geopolitical tensions impacted logistics through the Strait of Hormuz. Higher insurance, tariffs, and freight costs contributed to upward pressure on U.S. aluminum values. Copper inventories continue to grow even as prices remain elevated—an unusual combination that may signal market confidence and anticipated demand.

Stainless and Alloy

Nickel pricing on the LME has remained within a narrow range over the past month. Stainless grades 304 and 316 have shown modest improvement due to tighter supply conditions, though 316 momentum has been limited by molybdenum pricing resistance. Chrome-bearing grades may also see small gains as carbon steel values hold steady.

High-temperature alloy demand remains steady across aerospace, oil and gas, and defense markets. Although pricing remains subdued relative to intrinsic costs, expectations for gradual strengthening continue. Titanium markets show no signs of near-term recovery but remain stable due to consistent consumption.

Tool steels and high-speed steels remain stable, though molybdenum- and tungsten-bearing high-speed grades show incremental improvement. Carbide prices continue to rise amid reduced mining quotas and tighter export controls from China. Ongoing geopolitical tensions, including activity involving Iran, may introduce additional volatility.