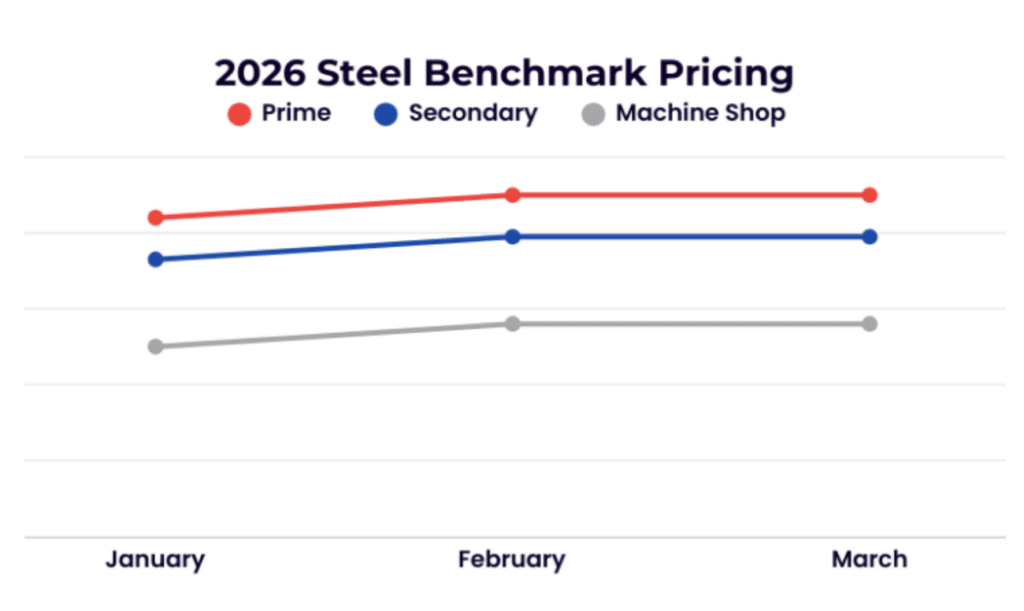

I hope you had a great weekend. As we move into March, several key metal markets are stabilizing following recent volatility. However, aluminum and some nickel based alloys have shown continued increases in strength.

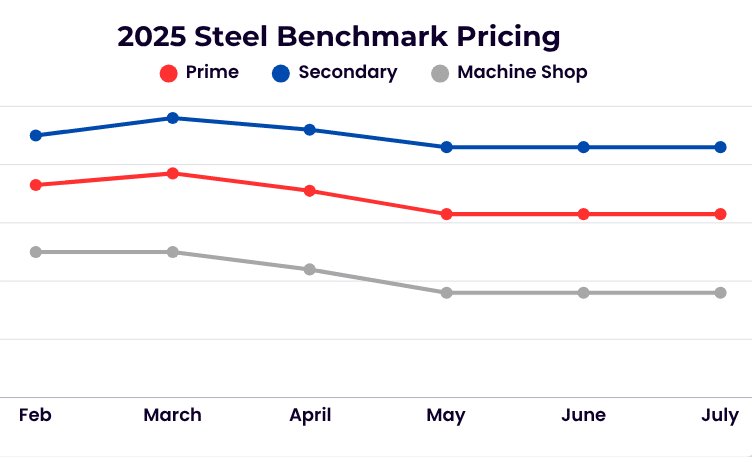

Steel

The U.S. steel scrap market remained steady in March. Supplier and mill delays from February created a supply-driven need for stability. Despite expectations of softening as winter conditions improved, many suppliers still faced February backlogs, limiting their flexibility to accept lower pricing.

Non-Ferrous Aluminum prices increased sharply as geopolitical tensions impacted logistics through the Strait of Hormuz. Higher insurance, tariffs, and freight costs contributed to upward pressure on U.S. aluminum values. Copper inventories continue to grow even as prices remain elevated—an unusual combination that may signal market confidence and anticipated demand.

Stainless and Alloy

Nickel pricing on the LME has remained within a narrow range over the past month. Stainless grades 304 and 316 have shown modest improvement due to tighter supply conditions, though 316 momentum has been limited by molybdenum pricing resistance. Chrome-bearing grades may also see small gains as carbon steel values hold steady.

High-temperature alloy demand remains steady across aerospace, oil and gas, and defense markets. Although pricing remains subdued relative to intrinsic costs, expectations for gradual strengthening continue. Titanium markets show no signs of near-term recovery but remain stable due to consistent consumption.

Tool steels and high-speed steels remain stable, though molybdenum- and tungsten-bearing high-speed grades show incremental improvement. Carbide prices continue to rise amid reduced mining quotas and tighter export controls from China. Ongoing geopolitical tensions, including activity involving Iran, may introduce additional volatility.

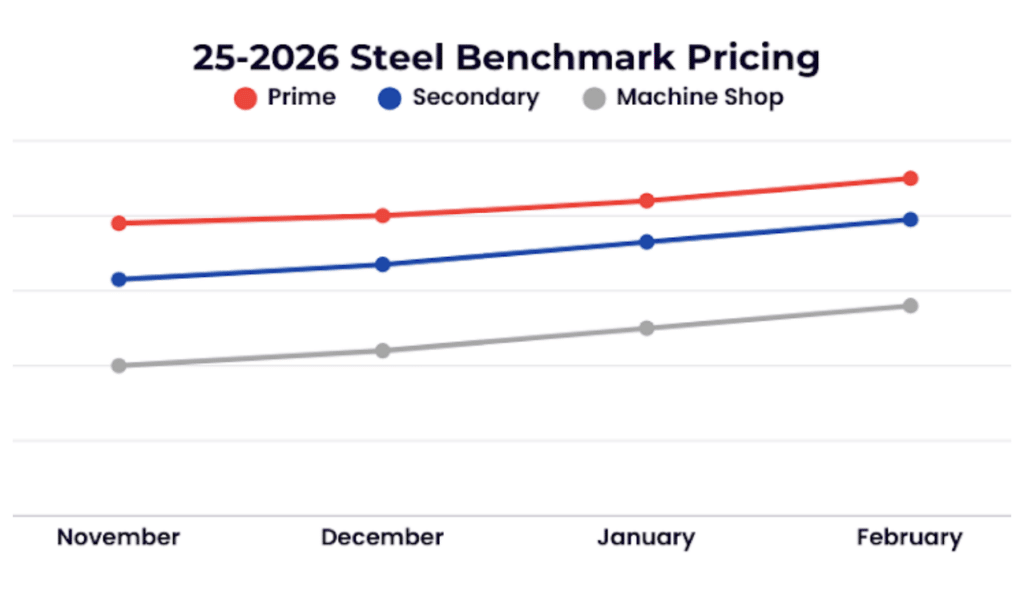

I hope all is well there. February continues to show strength in current markets with supply being an lackluster in a few sectors.

Steel

For the 3rd consecutive month, steel rose across all grades with increased steel production this February. European export markets kept pricing up after seeing US domestic prices rise. The moderate increase is attributed to slow inbound scrap flow. US vehicle sales hit a 3-year low last month and Japanese automaker Toyota lowering its global sales forecast with low consumer confidence.

Non-Ferrous The copper scrap market continues to demonstrate resilience in early February, with modest gains and overall stability across several key grades. The U.S. market remains relatively steady; however, international conditions tell a different story. China and India have seen notable declines, contributing to a softer global backdrop despite U.S. stability.

Buying activity in China has slowed significantly, and inventories on the Shanghai Futures Exchange continue to rise in a typical seasonal build ahead of the Lunar New Year. Even with this global cooling, copper prices remain nearly 29% higher than a year ago, supported by strong long-term demand from energy-transition initiatives and AI-driven infrastructure expansion.

The aluminum scrap market is showing mixed to weaker performance, with several indicators pointing toward mild downward pressure heading into February. As with copper, global industrial activity has softened—particularly in China as the country winds down operations ahead of the holiday period. Reduced mill demand has also pushed down spot pricing for primary aluminum grades.

While short‑term sentiment leans bearish, the structural, long‑term outlook remains stronger due to the continuing importance of recycled aluminum in manufacturing and ongoing supply constraints in primary production.

Stainless and Alloy

LME nickel is trading approximately $0.30 above the current spot market on a 30-day basis. While Indonesia has communicated prospective production cuts for 2026, the prevailing analyst consensus continues to call for a market surplus into next year, limiting upside momentum. 304 and 316 stainless pricing remains largely stable, with slight softness emerging as mills resist higher input costs amid relatively flat demand. Chrome-bearing stainless grades are holding for now, though modest pressure could develop as higher steel pricing provides near-term support.

High-temperature alloys are showing incremental improvement, though pricing has yet to realign with LME intrinsic values. Demand continues to exceed available supply, supported by persistent aerospace production backlogs, which remain elevated. Looking ahead, the outlook points to steady, sustained growth over the coming months, rather than an accelerated rebound.

The titanium market remains subdued, still working through lower-priced material released in 2025. Despite consistent demand across aerospace, industrial, medical, and energy sectors, many market participants believe a meaningful pricing correction may not materialize until Q1 2027.

Tool steels and high-speed steels are modestly firmer, underpinned by strength in cobalt and molybdenum pricing. Meanwhile, carbide drills and inserts continue to exhibit gradual price improvement, though increases remain measured as the market advances cautiously.

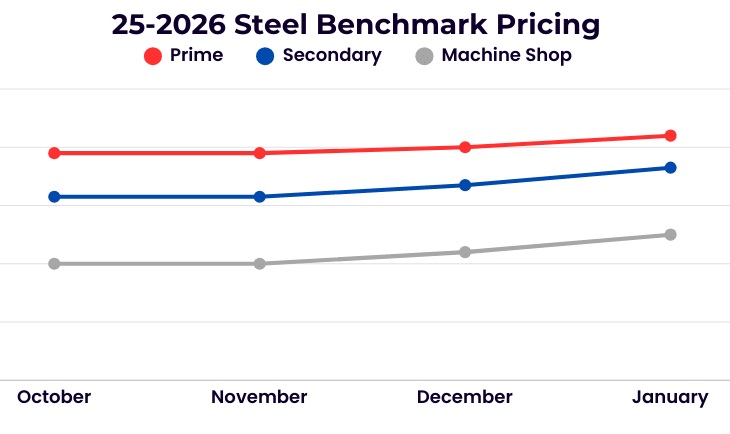

I hope you had a wonderful holiday season. Here’s a quick recap of USM’s extraordinary year of growth in 2025. We expanded our capabilities with a new aluminum briquetting line and an additional wire processing line, increasing efficiency and throughput for challenging materials. Masters and Alloys thrived, driven by strong precious metal markets. USM Processing achieved a record year for UBC processing despite a tough aluminum market, and USM Charter Alloys also posted another record year. USMe also saw significant growth, further strengthening our platform. Thank you to our industry partners for making this an incredible year.

Steel

January saw a continuation of December’s increases in ferrous. Once again prime scrap rose modestly, while cut grades experienced stronger gains. Busheling was expected to show more strength; however, global markets have been mixed with Turkey being the most active buyer, but China’s domestic scrap prices softened on sluggish steel demand and thinner trading.

Non-Ferrous The aluminum MWTP continues to rise and hits price records almost daily with the premium on the steps of $1.00. One UBC (used beverage can) mill confirmed out of the market for this year, and other mills have stated they’re easily buying at lower price levels due to the increased supply that’s available. Argus Media reports that rising consumption forecasts have contributed to the rising aluminum (LME) and copper (Comex) prices. China’s plans to implement in-depth measures to boost consumption, expand green electricity generation, advance urbanization and revive investment as notable priorities. While the US has shifted volumes away from China to other copper export markets at increased levels, the US is still experiencing weak domestic demand.

Precious Metals

Record-high gold prices also helped strengthen sentiment across the base metals complex. London gold futures broke through the $4,600/oz mark for the first time on Monday, driven by rising risk-aversion sentiment. Visit our Masters’ & Alloy site to view more about gold and other precious metal refining.

Stainless and Alloy

LME nickel showing support, with pricing trading roughly $0.50 higher over the past 30 days. Indonesia—the dominant global producer—has signaled potential production reductions beginning in late Q4 2025 for 2026, though the magnitude of these cuts has yet to be defined. Despite this supportive headline, the market remains cautious as global inventories continue to exceed demand. Another moderating factor in the current rally is the anticipated slowdown and structural shift in EV demand, which has tempered enthusiasm for sustained nickel price appreciation. Stainless steel pricing across all grades has edged modestly higher; however, increases have lagged the recent nickel movement. Mills remain hesitant for now, opting to see whether the rally proves durable before implementing further price adjustments. Chrome-bearing stainless grades, meanwhile, are holding firm.

High-temperature alloys have also shown some improvement, loosely tracking nickel’s recovery, though prices remain well below their respective 52-week highs. As the year progresses and demand visibility improves, additional upside may materialize.

Titanium markets continue to face significant challenges, as noted in prior monthly updates. Additional mills and producers have filed for bankruptcy amid unsustainable production costs and persistently weak market conditions.

Tool steels and high-speed steels remain relatively flat despite upward trends in molybdenum and cobalt. Carbide pricing, however, may face further increases as supply concerns persist. That said, any meaningful influx of supply could quickly halt momentum and lead to a rapid price correction.

As the year begins, ongoing uncertainty surrounding trade and tariff policies, political dynamics, production costs, labor constraints, and the continued war in Ukraine remain significant headwinds, making planning and forecasting increasingly difficult across the industry.

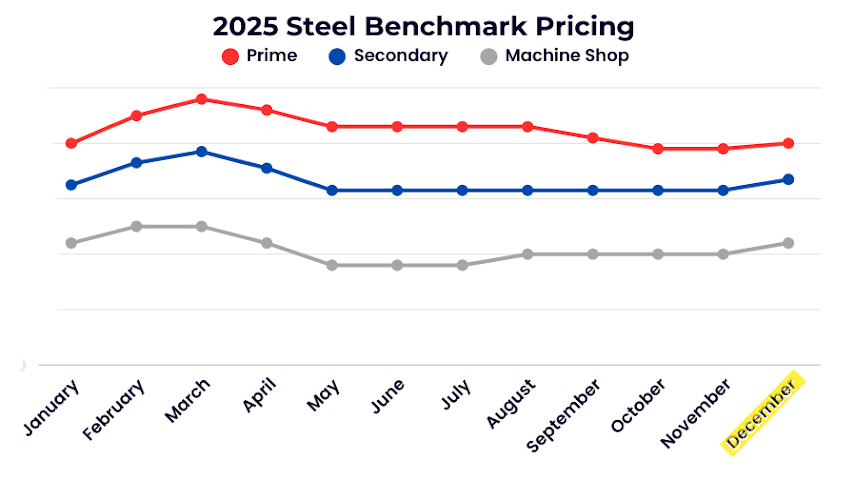

As we approach Year-End, we are reminded that our continued success would not be possible without our strong partnerships. Thank you for your commitment to our recycling programs—we look forward to entering 2026 with great possibilities. Now, for our final update of the year!

Steel

After several quieter months, the steel market saw pricing increase across the board to close out the year. Prime scrap rose modestly, while cut grades experienced stronger gains. Although weekly U.S. steel output has remained flat, seasonally slower inbound scrap flows and holiday disruptions tightened supply. What was expected to be a calm month shifted when a southern mill increased pricing to secure material for December, adding upward pressure across the market.

Non-Ferrous

Aluminum: The aluminum MWTP remains historically high, but weak demand continues to limit scrap price increases. Fire-related outages at Novelis’ rolling mill in Oswego, New York have contributed to an oversupply of aluminum, enabling other mills to purchase material at discounted rates.

Copper: Copper prices rose to record highs on the LME this week, while the Comex declined sharply ahead of the Federal Reserve’s interest rate decision. Concerns of an impending copper shortage in the export market are pushing LME pricing upward.

Stainless and Alloy

LME Nickel has traded within a tight range over the past month, yet stainless markets remain subdued due to persistently weak mill demand heading into the end of 2025. Grades 304 and 316 have seen modest pullbacks, with additional softening possible in 316 if Molybdenum continues to decline. While a few January inquiries have begun to surface, industry sentiment remains cautious, with limited signs of near-term recovery. In contrast, chrome-bearing stainless grades are showing relative stability, supported by firmer steel pricing this month.

High-temperature alloys may also see price reductions, influenced by lower Molybdenum values and seasonally soft demand. Although Cobalt continues its upward rally, alloy markets have yet to gain momentum as the year concludes.

Titanium markets remain muted, with sentiment still negative heading into 2026. In related news, two of the world’s largest aircraft manufacturers are finalizing a consolidation deal following a challenging year for one of the companies.

Tool Steels and High-Speed Steels continue to trend flat. Tungsten Alloys, however, have been setting record highs in recent months. While supply currently exceeds demand, pricing is still expected to strengthen in the near term. Even so, market participants remain cautious, aware that pricing could pivot quickly should sentiment shift.

Currently we’re seeing many manufactures as well as most mills and foundries enter the holiday season cautiously. US companies announced the largest job cuts (over 150,000) which is the highest for any October in over two decades.

Steel:

As expected the steel market went sideways on all grades. Consumers are currently trying to pressure buy prices downward, citing sluggish demand for finished steel and disruptions to construction activity caused by typhoons and flooding in Asia. However, some US consumers have noted a modest improvement in demand for some secondary markets.

Non-ferrous:

As the aluminum MWTP continue increase to new highs, some fabricators have switch to alternative material, such as magnesium, to decrease costs. Argus published that “purchases from aluminum producers are expected to slow in November because prices remain high and the industry has entered its off-season.” However, some manufacturers are expecting aluminum to continue to replace copper in some automotive and household appliance applications given the high copper prices.

The slowing global economy, particularly in China, has limited copper demand. China’s weak residential construction sector has been the key factor for the drop in demand, and their current number one priority is now artificial intelligence. As a result, copper spreads continue to widen based off the Chicago Mercantil Exchange with subdued trading expected during the holiday season.

Stainless and Alloy:

30-day LME Nickel has remained relatively stable, trending slightly below its recent average. However, stainless demand is expected to remain subdued through the remainder of 2025 due to typical year-end seasonality. 300-series, 316, and Chrome stainless grades have all recorded declines compared with the prior month. Adding to the uncertainty, ongoing economic headwinds have delayed U.S. mill contract negotiations—traditionally concluded in October—which are now anticipated to settle in November or December. Despite these challenges, the U.S. market continues to outperform Europe, supported by trade measures introduced in the second quarter that successfully curtailed inflows of low-priced imports.

High-temperature alloys segment, sentiment mirrors that of Nickel, with prices maintaining firm support amid year-end positioning. Select grades such as Inconel 625 and 718 are holding comparatively well, while less-utilized grades have softened. Cobalt continues to show a modest strength pattern, whereas Molybdenum remains under downward pressure, as previously highlighted in last month’s update.

Titanium market continues to face significant headwinds. Production delays from a major aerospace manufacturer—whose new aircraft program is now postponed until 2027—have dampened demand. Lower-grade Ferro Titanium has been particularly affected, with two of Europe’s largest mills recently declaring bankruptcy. Compounding this pressure is the declining use of Ferro Ti in automotive and steel applications, as automakers increasingly substitute aluminum for vehicle bodies and truck beds. Furthermore, the influx of cheaper Russian-origin Titanium units, often rebranded through third countries or blended into U.S. lots, is distorting market pricing. Mills broadly expect 2026 to mirror current conditions, with a tentative recovery not projected until Q4 2027.

In contrast, Tool Steel markets are showing resilience, with select grades containing Tungsten exhibiting strength. Tungsten-based alloys continue their upward trajectory, albeit at a slower pace, driven by tightening U.S. supply as export volumes remain elevated.

Overall, the alloy market remains in a state of cautious limbo. Year-end inventory management, economic uncertainty, and the pending outcome of tariff and trade policy decisions have left many manufacturers hesitant to commit fully to their procurement strategies heading into 2026.

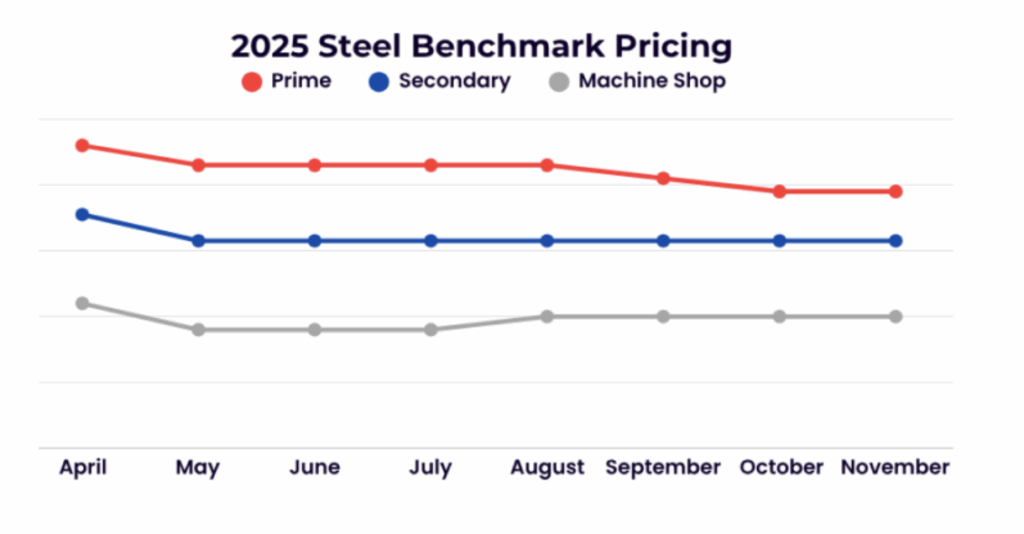

As we enter the 4th quarter, we’re reminded that Q4 has been a period of limited growth and lighter trading activity. This year, the uncertainty surrounding potential new tariffs and import duties makes forecasting even more challenging. Until clearer trade terms are established, manufacturing sectors are likely to remain cautious, limiting material intake as they prepare to enter 2026 with restrained confidence and measured inventory positions.

Steel:

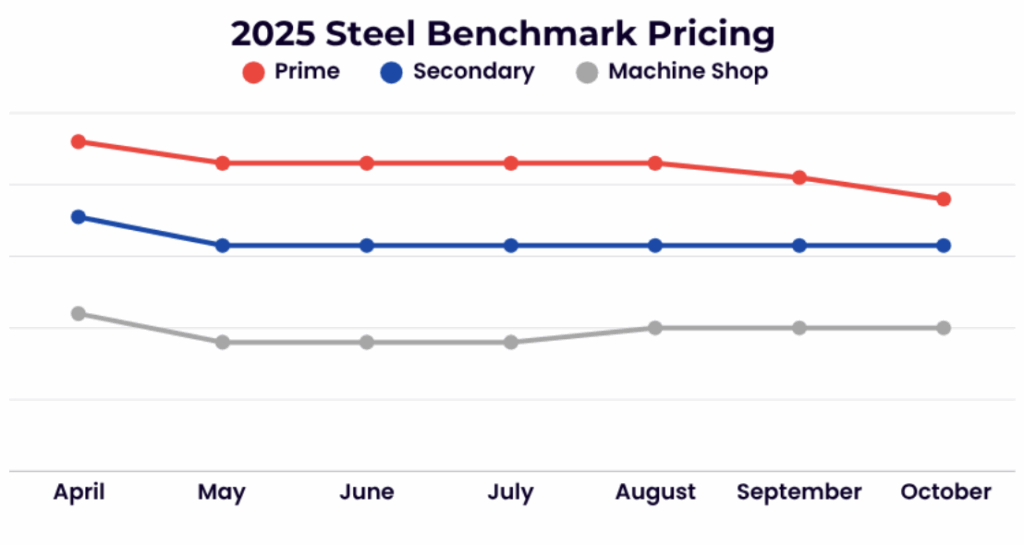

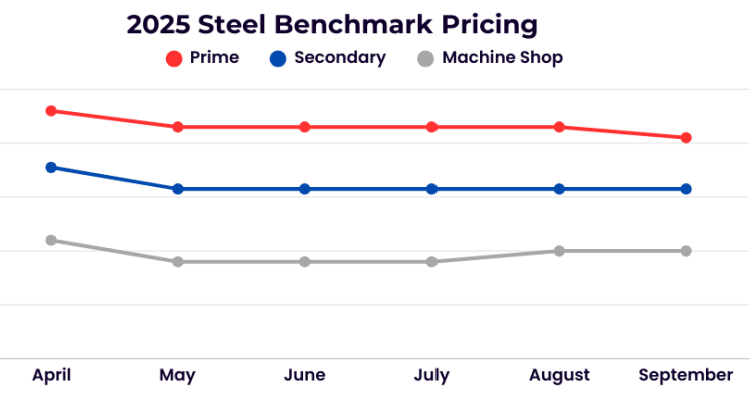

The steel market softened slightly this month, with prime, cut grades and shred grades declining $10-$20/GT. Demand remains sluggish in key sectors like construction and automotive, while global overcapacity—especially from new production in Asia—continues to weigh on prices. Trade policies and tariffs are also shaping the landscape, with both the U.S. and EU maintaining protectionist measures. Input costs for materials like iron ore and energy remain volatile, squeezing margins for producers. Analysts expect steel prices to stay relatively steady through the end of 2025, with potential for a gradual rebound in 2026 as demand slowly recovers.

Non-ferrous:

The growing arbitrage between the London Metal Exchange (LME) and Comex copper markets is once again causing wider copper scrap discounts in domestic and export markets, primarily driven by policy changes. This was previously observed in July 2025, following a tariff announcement that created historical spreads before being partially walked back.

Even as the LME and Midwest premiums hit record highs, the story on the ground feels a bit different. With inventories still running high and supply readily available, scrap prices have remained relatively steady—showing only minimal movement despite the broader market surge. Recent supply disruptions—most notably the major fire at a Novelis plant in September 2025—have further tightened parts of the market. At the same time, fewer aluminum outlets are only adding to the oversupply challenge, making an already complex situation even more difficult to navigate

Stainless and Alloy:

The LME has been trading within a notably tight range over the past month; however, weak mill demand continues to exert downward pressure on stainless grades. Compounding this softness, one of the major mills has temporarily halted operations for a three-week maintenance period. Grade 304 has experienced a more pronounced price reduction, with 316 following suit—partly due to the continued decline in Molybdenum values. Additionally, Q4 activity is subdued as many users seek to close out the year lean, avoiding excess inventory buildup.

High-temperature alloys are also trending weaker as demand continues to wane through the remainder of 2025. Mills are signaling reduced order volumes, reinforcing an overall cautious sentiment. While Cobalt prices are showing renewed strength, Molybdenum remains under pressure, and market participants have largely retreated to the sidelines. Cobalt’s gains may take additional time to translate into broader value improvements given the sustained softness in demand and prolonged floor-level trading. A slower-than-expected recovery in aircraft production has also constrained price movement across this segment.

Titanium markets remain unsettled, burdened by oversupply and postponed demand from aerospace and defense sectors. Although medium-term demand growth is anticipated, current production continues to outpace consumption. In anticipation of this slowdown, the world’s largest titanium sponge producer reduced output during Q3. At the same time, ongoing challenges related to tariffs and import duties have increased costs by as much as 60% in certain cases, significantly eroding profit margins.

Tool steel values remain relatively steady, while high-speed steels may find modest support from firmer Cobalt prices. Nevertheless, a more substantial rebound in manufacturing activity will be needed to sustain any meaningful upside. Tungsten carbide values, which had seen notable increases earlier in the year, appear to be stalling as Chinese market support has softened for two consecutive weeks.

I hope all is well there! We’re seeing some market stability heading into September. However Q4 sentiment has cooled, with recovery expectations pushed into early 2026. Consumers and mills are anticipated to re-enter the market with renewed appetite. However, lingering uncertainty around tariffs poses a potential drag on both demand forecasts and anticipated delivery schedules.

Steel:

Breaking last years trend of sideways movement to the end of the year, prime scrap dropped after standing still for 4 months. Reduced prices for mill sales along with an abundance of prime scrap available led to this months drop. Cut grades went remained the same and are expected to continue the trend in October. However, there’s anticipation of some life going into the final 2 months.

Non-ferrous:

US president Donald Trump has stated he will lower tariffs on EU-manufactured cars and auto parts to 15% as part of a trade agreement with the European bloc, but the effective date has yet to be determined. The copper arbitrage between the LME and Comex has remained close during the past month leading to improved copper spreads. Future copper consumption for increased US data centers to support AI will help keep prices stable and at some point, increase well as continued construction is maintained and grows.

The aluminum market has been relatively quiet internationally with the US Midwest aluminum premium maintaining its historic high. Consumers normally start to discuss next year’s orders over the next month. Due to future uncertainty, negotiations are currently being delayed until there is clarity regarding global tariffs, which will result in a longer review period.

Stainless and Alloy:

LME Nickel has remained confined within a narrow trading band over the past month. Stainless grades 304 and 316 are holding firm but could experience modest downward pressure in October as mill orders soften. Chrome stainless grades appear comparatively stable for the moment, though that stability may shift as additional mill guidance emerges.

High-temperature alloys continue to exhibit weakness, with consumers and mills alike deferring deliveries. Ample supply remains in the market, adding further weight to prices. Last month’s optimism surrounding a Q4 aerospace rebound has since diminished, with analysts now pushing expectations of renewed strength into Q1 2026.

Titanium markets remain unsettled, with abundant supply driving continued price volatility. The aerospace and aviation sectors have delayed activity, while steady scrap flow sustains downward pricing momentum. Since reductions began in April 2025, certain titanium grades have fallen nearly 15% from their 12-month highs. A meaningful recovery may prove a longer journey, with a rebound not anticipated until closer to the end of Q2 2026.

Tool steel values remain largely stagnant, though tungsten carbide pricing shows encouraging signs of improvement. China continues to absorb much of the scrap produced but has been slow to reintroduce units into the global market—a key factor supporting elevated values.

Following last years trend the steel market moved sideways for the fourth consecutive month, with the exception for the slight increase in turnings. While steel exports to some countries remain steady, it is lower than 2024 at this time and earlier this year. There is still some confidence that demand will heat up as we enter the fourth quarter.

Non-ferrous:

President Trump’s early July copper tariff announcement created a bearish market resulting several US mills looking to pivot to LME copper for stability and lower international pricing. After a month of widening consumer spreads, Comex dropped to the LME copper level once the US Proclamation was released, make the 2 markets aligned. The is still a large surplus of copper in the US; however, some mills are starting to heat up and taking orders.

Argus Metals reported that aluminum mills are still seeing current pricing drop steeper than the LME with continued oversupply. Consumers stated they’re well stocked through September and are looking towards October for deliveries.

Stainless and Alloy:

The 30-day LME Nickel average continues to trend in line with last month, maintaining relative stability with a slight downward drift. Stainless grades 304 and 316 remain largely flat; however, 316 may see modest upward movement, supported by a recent uptick in Molybdenum pricing and emerging concerns over supply. The Molybdenum rally has been further pressured by the imposition of higher reciprocal tariffs from the U.S. Chrome stainless grades remain stable for now, generally tracking alongside the broader ferrous market, which continues to move sideways.

High-temperature alloys have seen a continued softening in value, following the light retreat in Nickel and persistent weakness in the Cobalt market. That said, there are encouraging signs that aerospace demand is beginning to rebound—an encouraging signal that could lend support and possibly reverse the trend in pricing for these specialty alloys.

Titanium demand remains subdued, though a sustained recovery in the aerospace sector could help stabilize values in the near term. Analysts anticipate clearer signals as we approach the next fiscal year, when expected order flow may begin to materialize.

Tool steels and high-speed steels continue to face lackluster demand with little price movement to note. In contrast, carbide demand is robust, and pricing may trend upward. That said, volatility remains high—any easing in tariff-related pressures could quickly shift momentum, so buyers are advised to approach cautiously.

Overall, much of the market is maintaining a steady but cautious posture, as the broader industry awaits clarity on evolving tariff developments. The prospect of additional tariffs being implemented by month-end remains a significant factor, continuing to disrupt planning and confidence across the manufacturing sector.

I hope you had a wonderful holiday weekend! This month we’re still seeing the normal summertime lull for steel, experiencing another shakeup in the non-ferrous markets. Market sentiment overall remains cautious. The evolving landscape of global tariffs and potential trade negotiations is casting uncertainty over long-term planning and making it increasingly difficult for some manufacturers to conduct business with confidence.

Steel:

The steel market moved sideways again for the third consecutive month. Last year at this time we were gearing up for seven consecutive months of repeat pricing before the market showed signs of life this past January. Domestic and international weak markets along with ample scrap availability ultimately prevented upward movements in prices this month that some recyclers were initially expecting.

Non-ferrous:

Chinese buyers continue to show little interest in US copper scrap due to their ongoing sluggish economy and struggling real estate market. Combined with the wide arbitrage between the Chicago Mercantile Exchange and the London Metal Exchange, domestic consumers are still pricing and historically high copper spreads. President Trump’s July 9 tariff negotiation deadline has been contributing to a bearish market. Argus Metals states that “He began delivering letters on Monday to countries that detail their new ‘reciprocal’ tariff rates if trade negotiations fail to yield an agreement.” However, the recent 50% copper tariff announcement has sent Comex copper running up, while the LME copper declines.

Aluminum rolling mills continue to lower their buying prices with weaker demand. The soft interest for used beverage cans (UBC) is coupled with some mills quoting for September delivery. We’re also seeing a larger decrease in the smelter grade aluminum scrap that is associated with the domestic decrease in the automobile industry.

Stainless and Alloy:

The 30-day LME Nickel average has remained relatively steady to slightly down, showing resilience compared to other commodity markets that have been more visibly impacted by newly imposed tariffs. Stainless grades 304 and 316 continue to hold firm, buoyed by recent declines in scrap flow. However, 316 may experience upward pricing pressure as supply tightens in Molybdenum concentrates. Chrome stainless grades remain stable for the time being, perhaps benefiting from the broader steel market’s sideways movement.

High-temperature alloys have seen a modest decline, reflecting the subtle downward trend in their underlying input markets. Encouragingly, demand has proven more robust than expected heading into July, providing some support against further erosion in value.

In contrast, Titanium grades continue to soften, particularly select prime material, as labor tensions escalate in Europe. A pending strike vote by members of the European Unite union—spurred by disputes over inadequate pay—could lead to production delays and disrupt Airbus delivery schedules, casting a shadow over an already fragile sector.

Tool steels, high-speed steels, and Tungsten alloys are poised for potential price increases, with recent import duties reducing the availability of these goods in the U.S. market.

This month we’re still seeing uncertainty surrounding trade tariffs which continue to cast a shadow over procurement strategies. Some consumers remain hesitant to commit to additional volumes, and overall confidence heading into Q3 is muted. Without a clear resolution on tariffs and market volatility, near-term strength appears unlikely on some of the commodities.

Steel:

The steel market has hopefully bottomed out with all grades moving sideways for June. While consumers were anticipating lower steel prices on shred and cut grades, some stronger buying programs across the Midwest steel mills helped to boost prices to remain the same as last month. This likely helped to absorb a portion of the overhanging scrap in the market. Seeing an increase in futures trading promises some hope for a stronger July market.

Non-ferrous:

The US increasing aluminum and steel tariffs from 25% to 50% has created an international stir. The Midwest Premium jumped to record levels last week once the additional tariffs were determined, driving pricing to unprecedented heights. As a result, aluminum mills lowered their buying prices to offset the rapidly rising MWTP. Several UBC (Used Beverage Can) mills are full for June and July, with abundant supply and limited availability until at least August. Rest assured, being the largest UBC processor in North America, USM contracts allow us to continue to process and deliver all of our material as scheduled.

Copper spreads continued to widen the past week during some Comex swings and tepid domestic demand. Large copper scrap volumes are remaining in the US with consumers still not showing a real demand. There is a growing concern that copper may be next in line for an increased tariff and that fallout that we’re seeing with aluminum.

Stainless and Alloy:

LME Nickel continues to trade within a narrow range, yet demand has become increasingly insufficient. This weakening appetite has applied downward pressure on pricing, with notable discounts emerging across 304 and 316 stainless grades. Chrome stainless is similarly trending lower, driven by ongoing decline in iron values this month.

High-temperature alloys remain relatively stable, sustained by selective demand. However, market sentiment suggests that supply may soon outpace forecasts, particularly as consumers approach inventory thresholds.

Titanium grades continue to soften amid persistent demand weakness, compounded by a consistent influx of lower-cost Ferro Titanium, which is steadily accumulating in the market.

Tool Steel, High-Speed Steel, and Tungsten alloys remain firm. However, pricing may trend upward in the near term, as ongoing tariffs and constrained global flows tighten domestic supply and create upward pressure.

I’d like to share that once again we are ranked among North America’s 20 largest Non-ferrous recyclers in North America. Recycling Today has bestowed us with this honor consecutively since 2005. Thank you for your partnership and your choice to recycle responsibly with us!