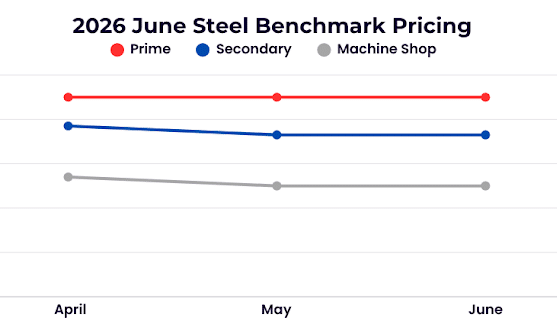

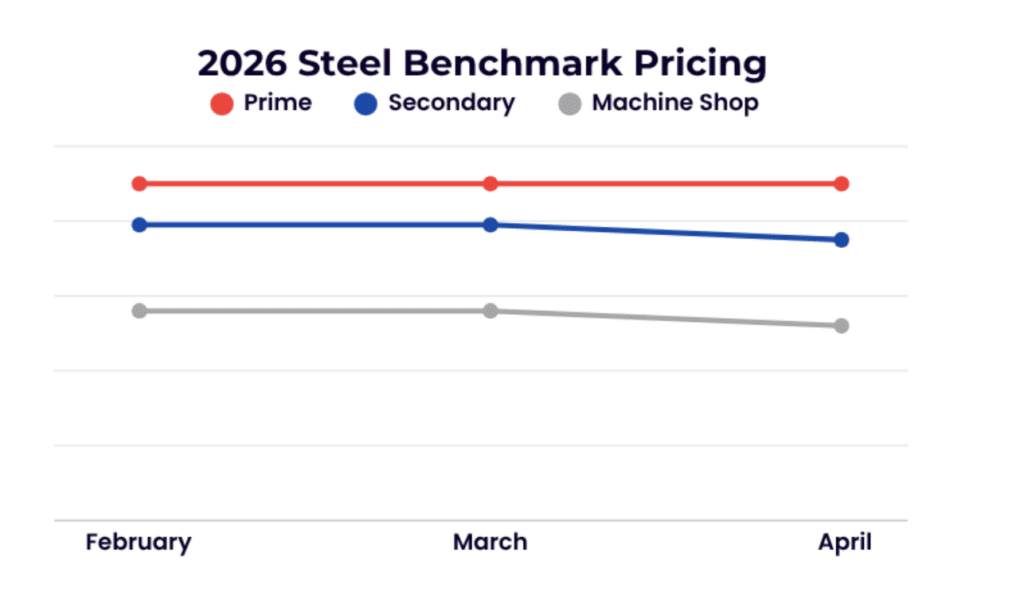

June market conditions reflected a continuation of the steady but fragmented environment established in May, with ferrous scrap prices largely trading sideways and nonferrous metals showing mixed but generally supportive trends. Across the U.S., scrap markets entered the summer period with balanced supply and demand fundamentals, as mills maintained stable purchasing patterns and avoided significant price adjustments. Market sentiment remained divided, with some participants expecting modest gains while others anticipated continued sideways movement, reinforcing the overall lack of a strong directional driver to start the month.

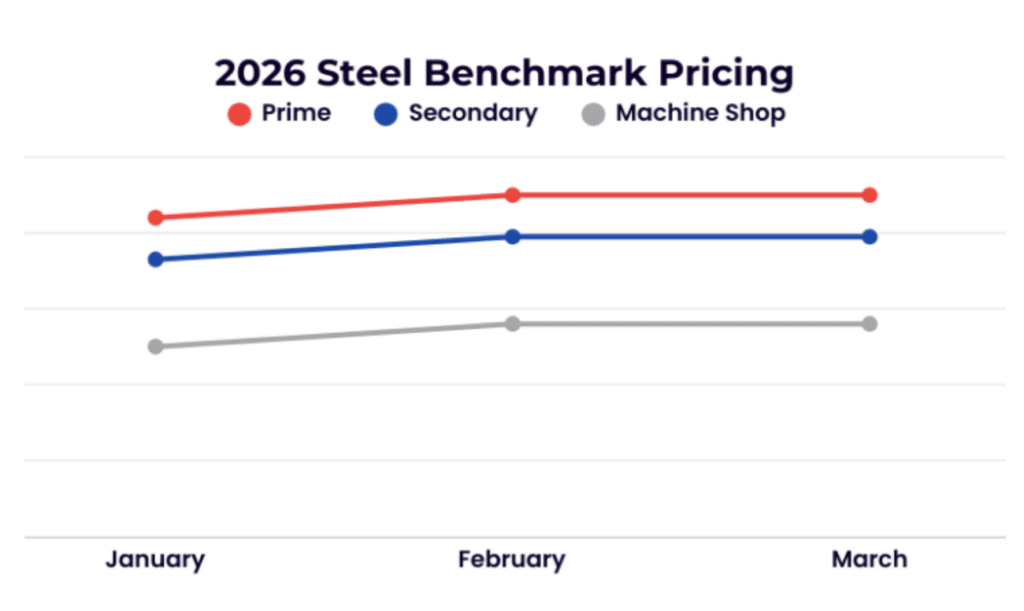

Steel

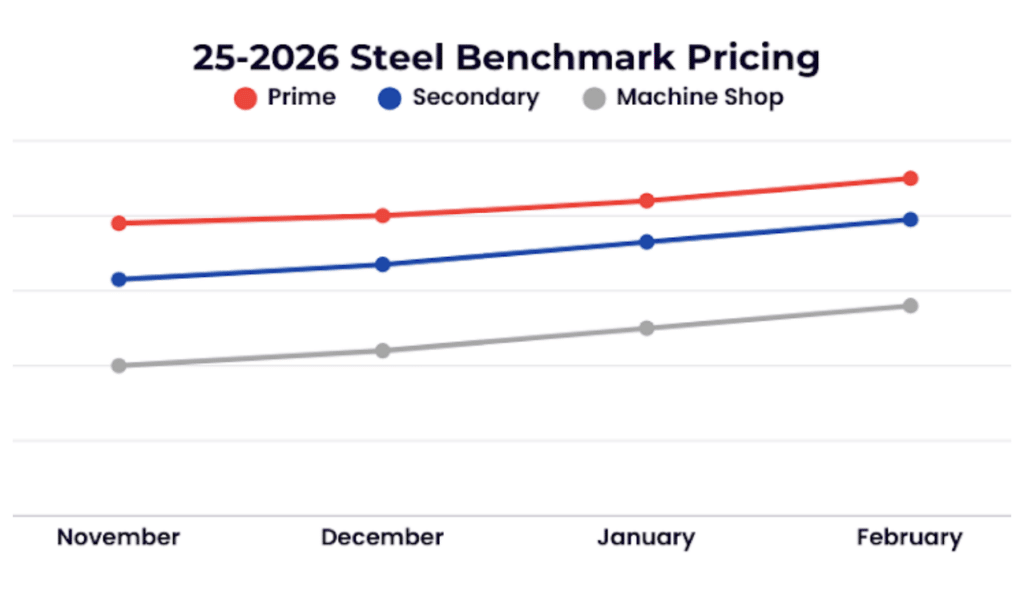

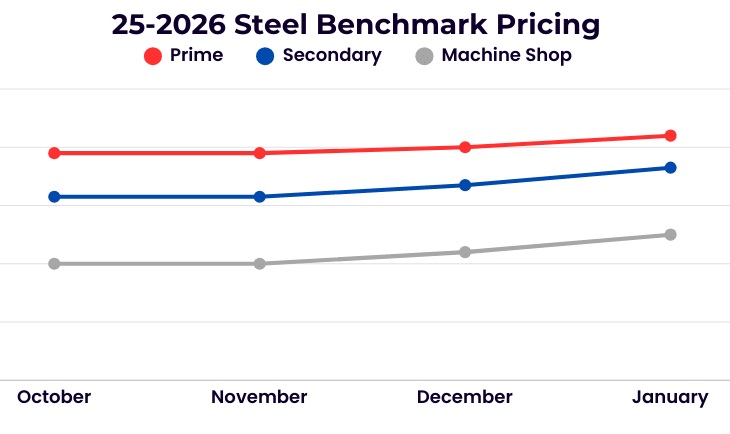

In the ferrous market, pricing across major grades—including shredded scrap, HMS, and busheling—held largely unchanged from May levels. Mills across multiple regions, including the Midwest, South, and Northeast, entered the June buying cycle at sideways pricing, reflecting adequate scrap flows and consistent procurement strategies. Supply conditions were stable, supported by improved seasonal inflows compared to earlier in the year, while mill inventories were reported near average levels, limiting the need for aggressive price movement. At the same time, strong steel production levels continued to support underlying scrap demand.

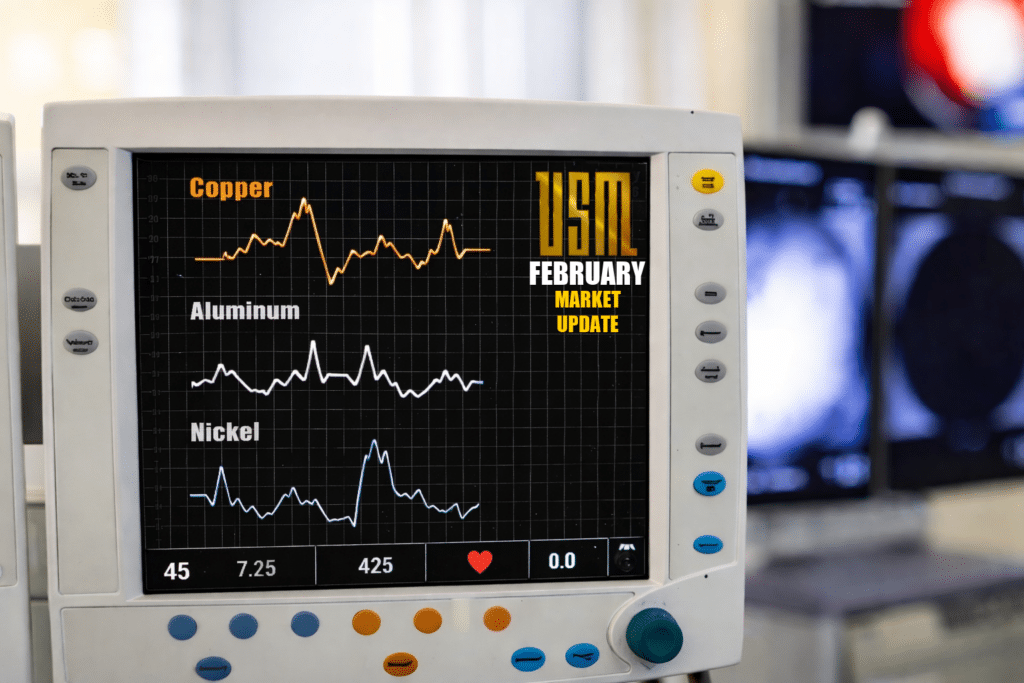

Copper

Nonferrous markets remained the primary source of movement in June, although trends varied by metal. Copper spreads between COMEX and the LME remained elevated in June due to ongoing arbitrage dynamics driven by regional pricing differences. COMEX copper continued to trade at a premium to global benchmarks, incentivizing traders to move physical metal into the U.S. to capture the spread. This has led to increased inventory levels domestically while drawing down supply in global markets. The divergence reflects a combination of U.S. demand strength, trade policy uncertainty, and logistics costs, resulting in wider domestic pricing versus export markets and continued volatility in copper scrap spreads. Demand continues to be supported by infrastructure, electrical, and industrial applications, although short term pricing remains sensitive to broader macroeconomic factors. Brass markets generally tracked copper, with modest gains reported across several grades, though pricing remained mixed depending on quality and regional demand.

Aluminum

Aluminum markets were more subdued, with most grades holding steady or declining slightly, reflecting balanced supply conditions and limited near term demand growth. UBC pricing followed this trend, but slightly lower as seasonal flows increased with aluminum mills already at capacity.

Looking ahead, the market enters the summer months with stable fundamentals but limited momentum. Ferrous scrap pricing is expected to remain largely rangebound unless driven by changes in steel production levels or export demand. Nonferrous markets—particularly copper—are likely to remain the most dynamic segment, with continued sensitivity to global commodity pricing and macroeconomic conditions. Aluminum and brass markets are expected to track broader trends in primary metals while remaining influenced by regional supply and demand conditions.

Stainless & Alloys

LME nickel fell by $0.30/lb over the past 30 days on profit-taking and softer industrial demand, while stainless still remains stable on steady consumption and balanced ferrous markets. 316 stainless may face near-term pressure as molybdenum prices ease and post-monsoon ore supply improves availability.

High-temperature alloys continue to be supported by strong aerospace demand outpacing production, despite some nickel-related softness, while titanium remains firm in prime grades as mills draw down inventories. Tool steels are broadly steady, with some pressure in high-speed grades but early signs of stabilization in carbide and tungsten as restocking begins.

Overall, demand from aerospace, defense, data centers, infrastructure, and batteries supports stainless and specialty alloys, though trade policy shifts and raw material risks will remain key pricing variables into 2H 2026.