April brought a partial reset in ferrous pricing, with obsolete grades moving lower and prime grades holding mostly steady. Nonferrous markets were firmer, led by copper strength and recovering aluminum pricing amid global supply concerns. Steel demand remained stable but uneven due to planned mill outages and early‐month buying discipline.

Steel

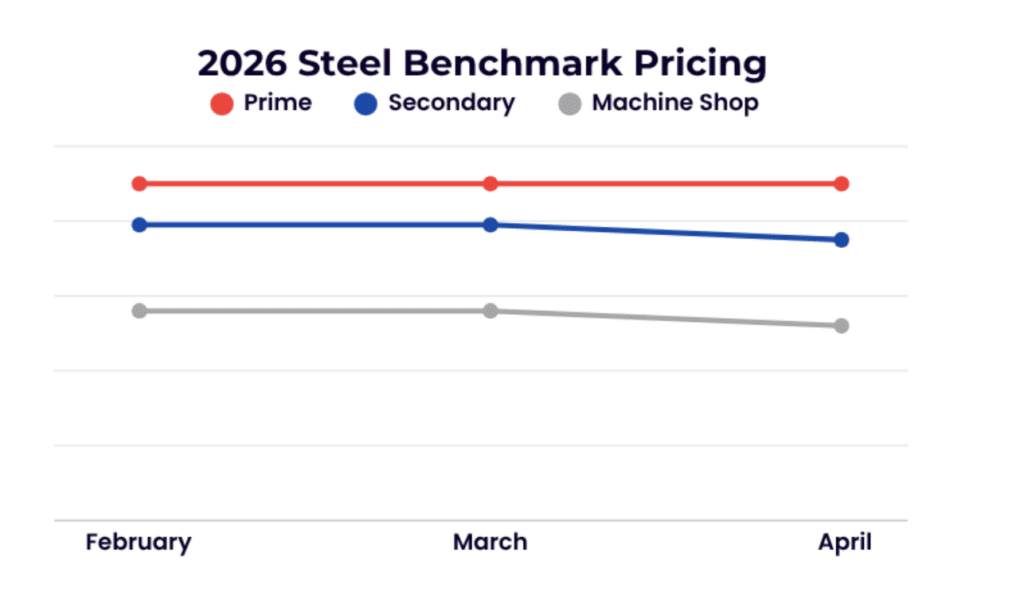

After a sideways March, the U.S. ferrous scrap market moved as expected, with obsolete grades coming under pressure amid improving seasonal flows and limited export demand. Prime grades proved more resilient, supported by steady domestic steel demand and stable finished steel pricing. Overall market sentiment remained cautious, as both buyers and sellers adjusted to a more balanced but uncertain environment.

Non-Ferrous

Nonferrous markets moved in the opposite direction, with copper leading the complex higher. Copper scrap prices strengthened through early April, tracking gains in refined copper markets and supported by structural demand from electrification, infrastructure investment, and ongoing geopolitical risks impacting global supply chains. Most copper grades posted gains, with particularly firm pricing in Bare Bright, #1 copper, and insulated wire categories. Aluminum markets were more mixed, but sentiment improved as primary aluminum prices surged in response to supply disruptions in key producing regions. While some aluminum scrap grades remained flat due to localized oversupply, higher underlying aluminum prices provided overall market support.

Stainless and Alloy

LME Nickel has traded within a notably narrow band over the past thirty days, lending a measure of stability to stainless steel markets, particularly across grades 304 and 316. This period of consolidation has provided a supportive backdrop; however, emerging softness in the broader steel complex suggests some near-term pressure. Chrome-bearing stainless grades may experience modest declines as consumers recalibrate pricing expectations in response to easing steel values. Similarly, grade 316 could face additional headwinds, with molybdenum retreating approximately 10% over the same period, eroding a key component of its cost support.

High-temperature alloys continue to demonstrate steady, if unspectacular, demand. That said, certain copper-bearing grades—most notably Monel—may encounter slight downward pressure, reflective of more tempered consumer interest. In contrast, vacuum-grade alloys such as Inconel 625 and 718 remain on firmer footing, with demand holding and pricing expected to remain stable barring any significant movement in the nickel market.

Titanium, despite a subdued outlook earlier in the quarter, appears to be regaining some traction. Mills have begun re-engaging in near-term purchasing discussions, which may provide a degree of support to ferro-titanium pricing. Nevertheless, higher-quality units, including 6-4 solids and turnings, have yet to exhibit meaningful momentum.

In the tool steel and high-speed steel segment, earlier optimism has softened. The rapid ascent in tungsten (Carbide) pricing dampened demand, prompting a pullback in buying activity. A corrective move in late February, triggered in part by China signaling a pause in further price increases, led to a wave of profit-taking and cautious positioning among traders. Compounding this, end-users are now working through elevated inventories accumulated in prior weeks. Current indicators suggest additional pricing pressure may persist in the near term.