Good Morning,

I hope you had a wonderful holiday season. Here’s a quick recap of USM’s extraordinary year of growth in 2025. We expanded our capabilities with a new aluminum briquetting line and an additional wire processing line, increasing efficiency and throughput for challenging materials. Masters and Alloys thrived, driven by strong precious metal markets. USM Processing achieved a record year for UBC processing despite a tough aluminum market, and USM Charter Alloys also posted another record year. USMe also saw significant growth, further strengthening our platform. Thank you to our industry partners for making this an incredible year.

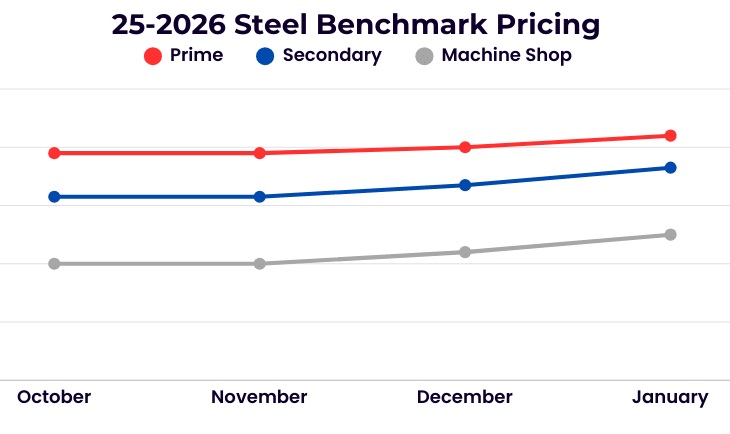

Steel

January saw a continuation of December’s increases in ferrous. Once again prime scrap rose modestly, while cut grades experienced stronger gains. Busheling was expected to show more strength; however, global markets have been mixed with Turkey being the most active buyer, but China’s domestic scrap prices softened on sluggish steel demand and thinner trading.

Non-Ferrous

The aluminum MWTP continues to rise and hits price records almost daily with the premium on the steps of $1.00. One UBC (used beverage can) mill confirmed out of the market for this year, and other mills have stated they’re easily buying at lower price levels due to the increased supply that’s available. Argus Media reports that rising consumption forecasts have contributed to the rising aluminum (LME) and copper (Comex) prices. China’s plans to implement in-depth measures to boost consumption, expand green electricity generation, advance urbanization and revive investment as notable priorities. While the US has shifted volumes away from China to other copper export markets at increased levels, the US is still experiencing weak domestic demand.

Precious Metals

Record-high gold prices also helped strengthen sentiment across the base metals complex. London gold futures broke through the $4,600/oz mark for the first time on Monday, driven by rising risk-aversion sentiment. Visit our Masters’ & Alloy site to view more about gold and other precious metal refining.

Stainless and Alloy

LME nickel showing support, with pricing trading roughly $0.50 higher over the past 30 days. Indonesia—the dominant global producer—has signaled potential production reductions beginning in late Q4 2025 for 2026, though the magnitude of these cuts has yet to be defined. Despite this supportive headline, the market remains cautious as global inventories continue to exceed demand. Another moderating factor in the current rally is the anticipated slowdown and structural shift in EV demand, which has tempered enthusiasm for sustained nickel price appreciation. Stainless steel pricing across all grades has edged modestly higher; however, increases have lagged the recent nickel movement. Mills remain hesitant for now, opting to see whether the rally proves durable before implementing further price adjustments. Chrome-bearing stainless grades, meanwhile, are holding firm.

High-temperature alloys have also shown some improvement, loosely tracking nickel’s recovery, though prices remain well below their respective 52-week highs. As the year progresses and demand visibility improves, additional upside may materialize.

Titanium markets continue to face significant challenges, as noted in prior monthly updates. Additional mills and producers have filed for bankruptcy amid unsustainable production costs and persistently weak market conditions.

Tool steels and high-speed steels remain relatively flat despite upward trends in molybdenum and cobalt. Carbide pricing, however, may face further increases as supply concerns persist. That said, any meaningful influx of supply could quickly halt momentum and lead to a rapid price correction.

As the year begins, ongoing uncertainty surrounding trade and tariff policies, political dynamics, production costs, labor constraints, and the continued war in Ukraine remain significant headwinds, making planning and forecasting increasingly difficult across the industry.