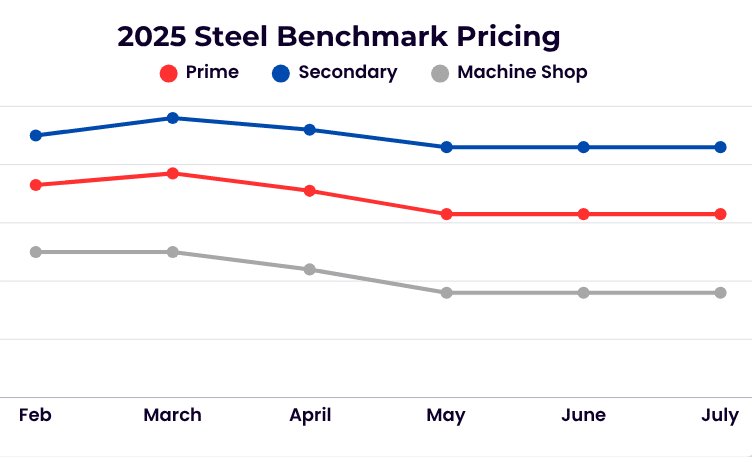

Steel:

Following last years trend the steel market moved sideways for the fourth consecutive month, with the exception for the slight increase in turnings. While steel exports to some countries remain steady, it is lower than 2024 at this time and earlier this year. There is still some confidence that demand will heat up as we enter the fourth quarter.

Non-ferrous:

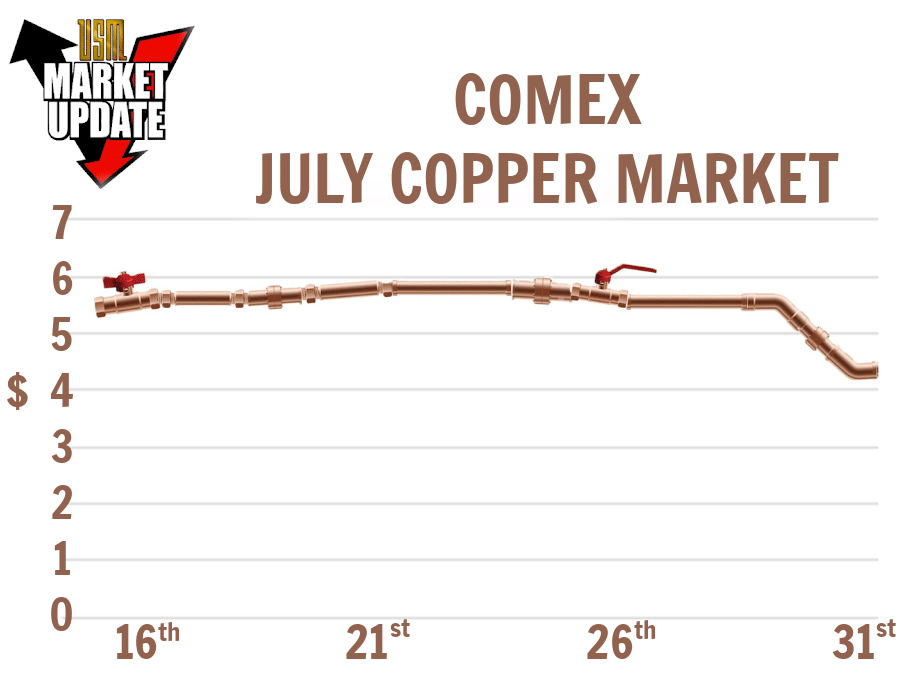

President Trump’s early July copper tariff announcement created a bearish market resulting several US mills looking to pivot to LME copper for stability and lower international pricing. After a month of widening consumer spreads, Comex dropped to the LME copper level once the US Proclamation was released, make the 2 markets aligned. The is still a large surplus of copper in the US; however, some mills are starting to heat up and taking orders.

Argus Metals reported that aluminum mills are still seeing current pricing drop steeper than the LME with continued oversupply. Consumers stated they’re well stocked through September and are looking towards October for deliveries.

Stainless and Alloy:

The 30-day LME Nickel average continues to trend in line with last month, maintaining relative stability with a slight downward drift. Stainless grades 304 and 316 remain largely flat; however, 316 may see modest upward movement, supported by a recent uptick in Molybdenum pricing and emerging concerns over supply. The Molybdenum rally has been further pressured by the imposition of higher reciprocal tariffs from the U.S. Chrome stainless grades remain stable for now, generally tracking alongside the broader ferrous market, which continues to move sideways.

High-temperature alloys have seen a continued softening in value, following the light retreat in Nickel and persistent weakness in the Cobalt market. That said, there are encouraging signs that aerospace demand is beginning to rebound—an encouraging signal that could lend support and possibly reverse the trend in pricing for these specialty alloys.

Titanium demand remains subdued, though a sustained recovery in the aerospace sector could help stabilize values in the near term. Analysts anticipate clearer signals as we approach the next fiscal year, when expected order flow may begin to materialize.

Tool steels and high-speed steels continue to face lackluster demand with little price movement to note. In contrast, carbide demand is robust, and pricing may trend upward. That said, volatility remains high—any easing in tariff-related pressures could quickly shift momentum, so buyers are advised to approach cautiously.

Overall, much of the market is maintaining a steady but cautious posture, as the broader industry awaits clarity on evolving tariff developments. The prospect of additional tariffs being implemented by month-end remains a significant factor, continuing to disrupt planning and confidence across the manufacturing sector.