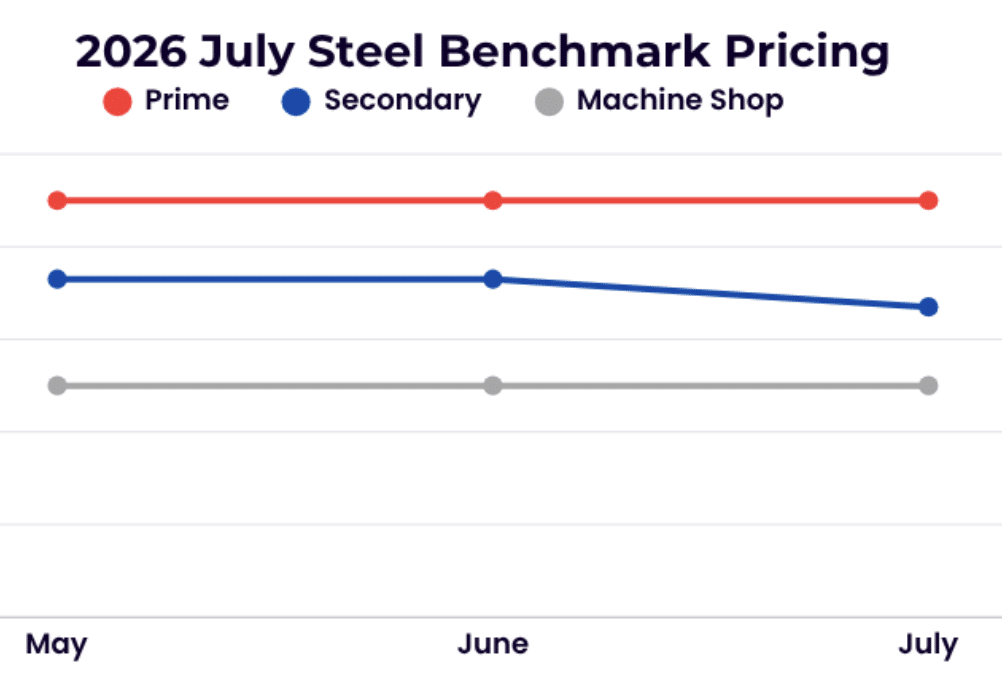

July market conditions remained generally stable, although sentiment softened across parts of the ferrous sector as seasonal mill outages, extreme heat, and summer operating schedules tempered demand expectations. Scrap availability remained adequate in most regions, and inventory levels were reported near historical averages, resulting in a balanced market without a clear catalyst for significant price movement. While buyers adopted a cautious approach, overall pricing remained relatively steady across most grades.

Steel

In the ferrous market, steel scrap prices remained largely unchanged through the first half of July as domestic mills maintained consistent purchasing patterns and continued operating at healthy utilization rates. U.S. raw steel production remained strong, with mills producing approximately 1.86 million net tons per week and operating above 80% capacity utilization. Year-to-date steel output remained roughly 6% above 2025 levels, supporting ongoing scrap consumption. However, weaker export demand, particularly from Turkey (the world’s largest scrap importer) continued to limit upside potential for obsolete grades such as shredded scrap and HMS.

Copper

Nonferrous markets were more constructive during July. Following June’s surge to record-high copper prices and the subsequent correction of approximately 10% later in the month, copper scrap prices stabilized and posted modest gains across most major grades in July. Market support continued to come from steady industrial demand, ongoing infrastructure investment, and strength in the underlying copper market. While month-to-date gains have been relatively modest, copper prices remain at historically elevated levels compared to long-term averages, providing continued support for copper scrap values.

Aluminum

Aluminum markets are starting to rebound somewhat during July after a mixed performance through much of the second quarter. Some secondary aluminum scrap grades posted gains, including Used Beverage Can (UBC) during the first half of the month as secondary aluminum demand improved experienced week-over-week gains. Despite these improvements, aluminum pricing remains dependent on broader primary aluminum trends and seasonal scrap flows.

Brass

Some Brass markets also moved higher during July, benefiting from copper’s strength. Both red brass and yellow brass prices recorded modest gains, reflecting stable demand from foundries and industrial consumers. Price increases remained measured, but the market continued to trend positively compared with the relatively flat conditions seen earlier in the summer.

Stainless Steel & Alloy

LME nickel traded approximately $0.60/lb below the June average, largely driven by uncertainty surrounding Indonesian export policies and supplier agreements. A softer market is anticipated over the next six months as participants monitor global demand trends and supply chain developments. 304 stainless pricing softened modestly, while 316 grades remained firm, supported by steady demand and molybdenum support. Chrome-bearing stainless grades have also held pricing for the time being.

Despite stable demand, high-temperature alloy pricing moved lower in line with nickel’s decline. Titanium pricing remained relatively steady, with increased market participation potentially supporting modest strengthening ahead. Tool steel and high-speed steel markets edged lower due to softer demand and seasonal summer slowdowns. The tungsten alloy market also weakened from the prior month as speculative inventories re-entered the market, pressuring demand.

Looking ahead, the market enters the latter part of summer with generally balanced fundamentals. Ferrous pricing is expected to remain stable barring significant changes in export activity or domestic steel production. Copper appears poised to remain the strongest nonferrous performer, supported by elevated COMEX pricing and ongoing infrastructure and electrification demand. Aluminum and brass markets are expected to continue tracking broader base metal trends while remaining sensitive to regional supply and demand conditions.